Reforms in a few countries drive a decline in average OECD labour taxes

Income tax and social security contributions declined slightly for the average worker across the OECD in 2018, driven by major reforms in a handful of countries, according to a new OECD report.

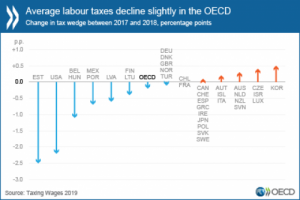

Taxing Wages 2019 shows that the “tax wedge” – total taxes on labour costs paid by employees and employers, minus family benefits, as a percentage of the labour cost to the employer – was 36.1% in 2018. This represents a fall of 0.16 percentage points from 2017, and is the fourth consecutive annual decrease in the tax wedge on the average OECD worker.

The decline between 2017 and 2018 was caused by large decreases in four countries: Estonia (2.54 percentage points), the United States (2.19 percentage points), Hungary (1.11 percentage points) and Belgium (1.09 percentage points). Even though the tax wedge on the average worker across the OECD declined between 2017 and 2018, small increases in the tax wedge were actually observed in 22 countries, or nearly two-thirds of the OECD. At the same time, small decreases in the tax wedge were observed in the remaining 10 OECD countries.

In the four countries where the largest decreases in the average tax wedge were observed, these reductions resulted from major reforms. In Estonia and the United States, the decreases were due to income tax reforms, whereas in Hungary and Belgium they resulted from reductions in employer social security contributions.

Taxing Wages 2019 also considers the net personal average tax rate, which measures the income tax and social security contributions paid by employees, minus any family benefits received, as a share of gross wages. In 2018, the OECD average rate was 25.5%. This OECD-wide average rate, calculated for a single person with no children earning the average wage, has remained stable in recent years, even though this rate varies considerably among countries: ranging from below 15% in Chile, Korea and Mexico to over 35% in Belgium, Denmark and Germany.

The 2019 edition of Taxing Wages also includes a Special Feature that looks at the taxation of the median worker in OECD countries, comparing this to the taxation of the average worker. In all OECD countries, the median worker has a lower wage than the average worker, due to higher differentials at the upper end of the income distribution. On average, the median worker earns 80.8% of the average wage and consequently faces a lower average tax wedge, at 34.3% compared to 36.1% for the average worker. This difference is primarily due to lower income taxes. However, the report shows that while providing a more comparable point in the wage distribution across countries, the median wage is difficult to calculate due to data availability, and the differences are not significant for most countries.

Key findings

Tax wedges for single people and families with children

In 2018, the highest average tax wedges for single workers with no children earning the average national wage were in Belgium (52.7%), Germany (49.5%), Italy (47.9%), Austria and France (47.6%). The lowest were in Chile (7%), New Zealand (18.4%) and Mexico (19.7%).

The highest tax wedge for one-earner families with two children at the average wage in 2018 was in France (39.4%). Austria, Belgium, Finland, Greece, Italy, Sweden and Turkey also had tax wedges over 37%. For this family type, New Zealand had the lowest tax wedge (1.9%), followed by Chile (7.0%) and Switzerland (9.8%).

The OECD average tax wedge for the one-earner couple has remained flat for the last two years, at 26.6%. The largest increases in the tax wedge for this family type in 2018 were in Poland (10.3 percentage points). There were no other increases over one percentage point. The largest decreases were in New Zealand (4.5 p.p.), Lithuania (2.5 p.p.) and Estonia and the United States (2.4 p.p.).

The tax wedge for one-earner families with children is lower than for single people without children in all OECD countries except Chile and Mexico, where tax levels are the same for both. The gap is over 15% of labour costs in Belgium, Canada, the Czech Republic, Germany, Ireland, Luxembourg, New Zealand and Slovenia.

Net personal average tax rates (NPATR) for single people and families

In 2018, the highest average NPATR for single workers with no children earning the average wage were in Belgium (39.8%), Germany (39.7%) and Denmark (35.7%). The lowest were in Chile (7%), Mexico (10.2%) and Korea (14.9%). The OECD average fell by 0.16 percentage points to 25.5%.

The average NPATR for one-earner families with children was 14.2% in 2018. The highest NPATRs for one-earner families with two children at the average wage were in Turkey (26.2%) and Denmark (25.2%). The lowest NPATRs were in the Czech Republic (0.2%), Canada and Estonia (both 1.8%).

Special Feature

The median wage refers to the worker at the 50th percentile of the wage distribution, whereas the average wage is the sum of full-time wages divided by the number of workers. The average is therefore more influenced by differentials at the upper end of the wage distribution.

The average tax wedge on median workers in 2017 ranged from 52.0% in Belgium to 7% in Chile. In 21 countries, the median worker faced a tax wedge of between 30% and 45%.

The average tax wedge for the median worker is lower than the average in all but two countries (Hungary and Chile) although changes are significant for only a few countries where the lower level of median wage resulted in reductions in allowances/employer SSCs and lower marginal personal income tax rates (Turkey, Luxembourg, Portugal, Italy, Israel and Ireland).

Source: Organisation for Economic Co-operation and Development

- 495 reads

Human Rights

Fostering a More Humane World: The 28th Eurasian Economic Summi

Conscience, Hope, and Action: Keys to Global Peace and Sustainability

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

Puppet Show I International Friendship Day 2020