IMF Executive Board Concludes Article IV Consultation with Guyana

On June 15, 2018, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Guyana and considered and endorsed the staff appraisal without a meeting.

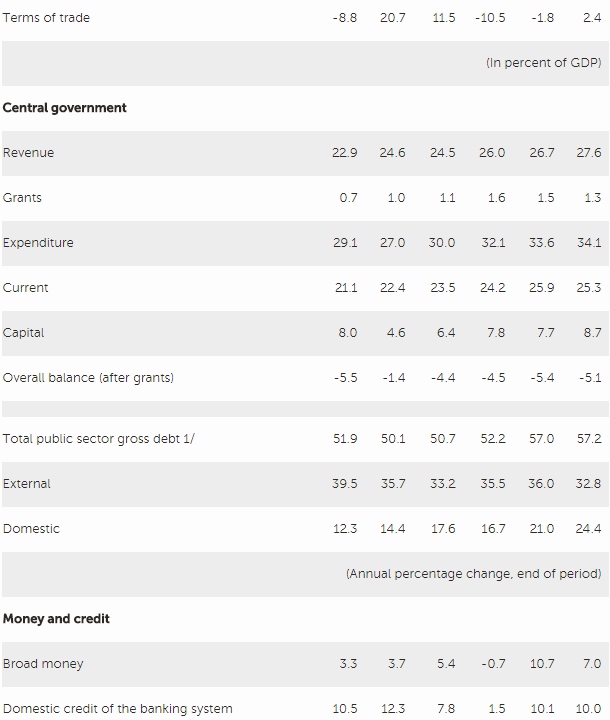

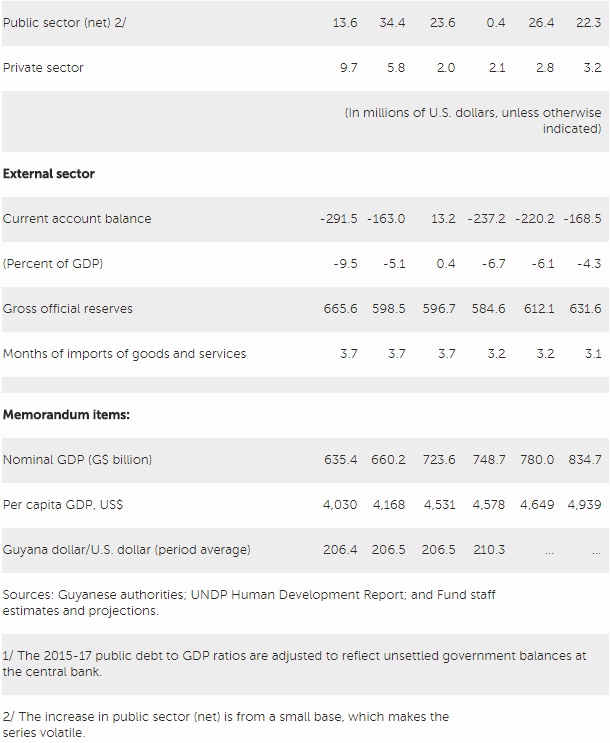

Economic growth slowed in 2017, but became more broad-based. The economy grew by 2.1 percent, down from 3.4 percent in 2016, on the account of lower than expected mining output and weak performance in the sugar sector. Nonetheless, non-mining growth rebounded to 4.1 percent following a contraction in 2016. Inflation remained stable at 1.5 percent at end-2017, largely driven by food items, while core inflation was close to zero. The external balance turned negative due to weaker than expected export growth and higher oil prices. In 2017, the current account recorded a deficit of 6.7 percent of GDP from a surplus of 0.4 percent in 2016. The financial account improved due to FDI, particularly in the oil and gas sector, and higher loan disbursements to the public sector. Gross reserve cover stood at 3.2 months of imports at end-2017. The central government’s deficit remained stable at around 4.5 percent of GDP in 2017. Improvements in tax administration contributed to a 1.2 percentage point increase in the tax revenue to GDP ratio, which was partly offset by a 0.4 percentage point decline in the ratio for non-tax revenue. Public debt stood at 52.2 percent of GDP at end-2017. Credit to the private sector grew 2.1 percent in 2017 due to a combination of weak demand and banks continuing to strengthen their balance sheets. Guyana’s banking system remains relatively stable. Although banks remain profitable and have adequate capital buffers, non-performing loans (NPLs) remain high at 12.2 percent of total loans at end-2017, down from 12.9 percent at end-2016.

Guyana’s medium-term prospects are very favorable. Oil production is expected to commence in 2020, and additional oil discoveries have significantly improved the medium- and long-term outlook. Economic growth is projected to be 3.4 percent in 2018, driven by continued strength in the construction and rice sectors, and a recovery in gold mining. The current account deficit is projected to narrow to 6.1 and 4.3 percent of GDP in 2018 and 2019, respectively. The deficit will be financed largely by FDI inflows and donor-supported investment. The central government deficit is projected to widen to 5.4 and 5.1 percent of GDP in 2018 and 2019 due to the cost of restructuring the sugar sector and an increase in infrastructure-related capital expenditure. Public debt is projected to rise in the short-term, before declining with the onset of oil production.

Executive Board Assessment

In concluding the 2018 Article IV Consultation with Guyana, Executive Directors endorsed staff’s appraisal as follows:

Guyana’s macroeconomic outlook remains favorable. While growth slowed down in 2017, it became more broad-based, and is expected to accelerate in the run-up to the start of oil production in 2020. The extractive industries and public investment will be key drivers of economic growth over the medium-term. Reducing the costs of doing business, strengthening private sector confidence, and advancing productivity-enhancing reforms are essential for sustaining growth in the short-term, and for reaping the full benefits of the oil windfall once it materializes.

Short-term financing needs should be carefully managed. The authorities’ prudence and restraint towards borrowing in anticipation of future oil revenue is commendable. They should rely as much as possible on Multilateral Development Banks, including their non-concessional financing operations. Developing the domestic capital markets would provide a more stable source of financing and help meet the needs of domestic long-term institutional investors. Private external borrowing should continue to be avoided, and central bank financing should not be used at all. Staff welcomed the authorities’ intention to close the overdraft balances at the central bank in the near-term. Saving the one-off gains from the tax amnesty would reduce financing needs, and also help preserve external buffers.

The quality and efficiency of government expenditure should continue to be improved. It is important to address the shortcomings identified by the PIMA before public investment is significantly scaled-up with oil revenues. For similar reasons, it would be useful to review current expenditures to ensure they achieve the maximum welfare and inclusion benefits.

The rules-based fiscal framework for managing oil wealth should be transparent and consistent with the resource fund deposit/withdrawal rules. It should provide the basis for determining the allocation of annual oil revenue for stabilization and domestic capital expenditure, as well as intergenerational savings. The consistency between the fund deposit/withdrawal rules and a fiscal rule could be reinforced by a fiscal responsibility legislation.

Monetary policy should gradually revert towards a neutral stance as the economic recovery gains pace, and inflationary pressures arise.

The exchange rate should play a more active role in cushioning external shocks going forward. Guyana remains vulnerable to external shocks given the concentration of its exports in a few commodities and its reliance on imported oil in the short-term. Over the long-term, building an adequate buffer stock of savings from the oil revenues would also help cope with external shocks.

Significant progress has been made in implementing the 2016 FSAP recommendations, but further progress is needed in some areas. Ensuring the internal consistency of supervisory function from routine supervision to intervention and resolution remains a priority. Other important areas where work still needs to be finalized include: eliminating reduced provisioning requirements for “well-secured” portions of NPLs; refining the definition of “related parties” with the international standards; reducing the reliance on overdraft lending; clarifying the upstream and downstream ownership of institutions; and raising minimum capital adequacy requirement to 12 percent; and reducing the banks’ large exposure limits.

Enhancing competitiveness and supporting inclusive growth should remain a high priority. Greater efforts are needed to lower the cost of doing business by addressing infrastructure-related bottlenecks, reducing energy costs, and cutting red tape. Increasing female labor force participation and bridging the gaps with the Hinterland can boost growth and help spread its benefits more widely.

Oil exploration and production should be included in the national accounts when they are rebased, and also in the BOP statistics. Strengthening external sector statistics and compiling an international investment position should be a priority.

Source: International Monetary Fund

- 300 reads

Human Rights

Fostering a More Humane World: The 28th Eurasian Economic Summi

Conscience, Hope, and Action: Keys to Global Peace and Sustainability

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

Puppet Show I International Friendship Day 2020