IMF Executive Board Concludes 2017 Article IV Consultation with Argentina

On December 18, 2017, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Argentina.

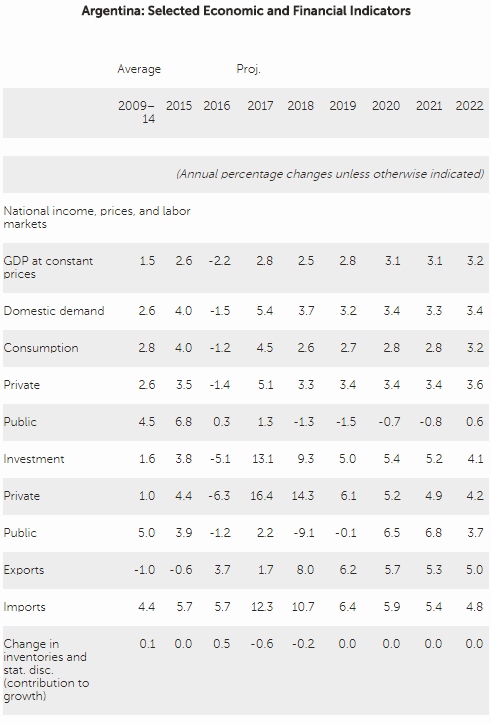

Argentina’s government has unwound multiple distortions and made important progress in restoring integrity and transparency in public sector operations. These policy changes have put the economy on a stronger footing and corrected many of the most urgent macroeconomic imbalances. Argentina is experiencing a solid recovery from last year’s recession and, even in the face of planned fiscal consolidation and ongoing efforts at disinflation, growth is expected to consolidate in the coming years. Inflation continues to fall, albeit at a slower pace than targeted by the central bank.

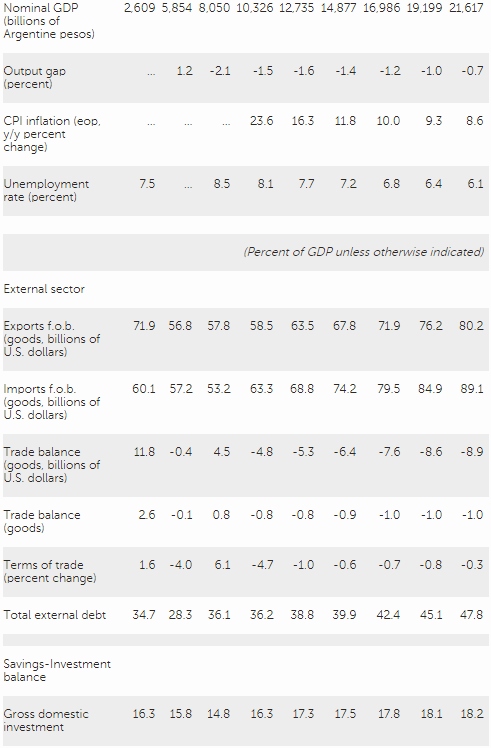

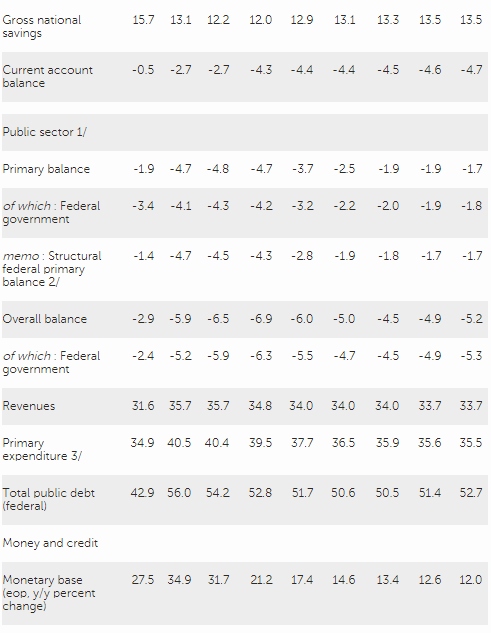

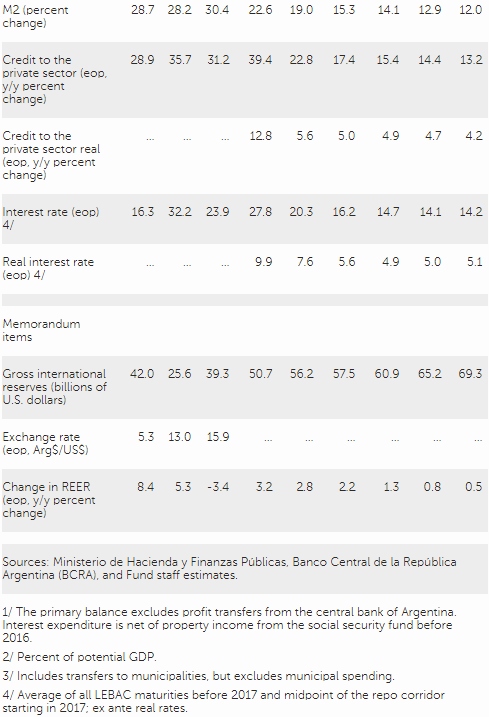

Private consumption strengthened in 2017, supported by greater real wages and buoyant credit growth, and private investment is also picking up. With stronger domestic demand, the trade surplus turned into a deficit and the current account deficit increased. Annual inflation has declined from its peak in 2016, but remained relatively resilient and inflation expectations moved up, prompting the central bank to raise interest rates. The general government fiscal deficit is expected to increase this year, despite the fall of the primary deficit, and its financing led to a rapid rise in foreign currency borrowing. The slower-than-targeted decline in inflation and significant foreign inflows have put upward pressure on the exchange rate, which in real terms has appreciated by about 3 percent so far in 2017.

Going forward, GDP growth is expected to consolidate, inflation inertia will slowly subside, and the fiscal deficit will gradually fall. Private consumption is expected to strengthen in 2018–19 as real wages recover from the decline in 2016. The federal primary fiscal deficit is expected to fall by 2 percent of GDP by 2019, while provinces are projected to lower their primary deficit, in line with the targets announced by the authorities. This is likely to weigh against economic growth in the next two years, holding it to around 2½ percent. Continued sizable foreign borrowing and real appreciation pressures of the currency are expected to cause the current account deficit to increase further. As wage negotiations continue to become more forward-looking, inflation expectations should move lower, creating space for an eventual reduction in policy rates. While still high real interest rates will act as headwind to growth, they should facilitate a decline in inflation towards single-digit levels.

Executive Board Assessment

Executive Directors agreed with the thrust of the staff appraisal. They welcomed the continuing recovery of Argentina’s economy from the recession that began in 2015. They commended the authorities for putting in place measures that facilitated the economic rebound, and for the progress made in the systemic transformation of the Argentine economy, including efforts to rebuild institutions and restore integrity, transparency, and efficiency in government. At the same time, they noted that important challenges remain and further efforts are needed.

Directors agreed that a lower fiscal deficit would reduce external vulnerabilities, build credibility, and help anchor inflation expectations. Many Directors supported a more frontloaded fiscal rebalancing, which would allow for lower interest rates, reduce upward pressures on the peso, and limit vulnerabilities to a sudden tightening of external financing conditions. A number of other Directors, while concurring with the need to reduce the fiscal deficit, also noted the potential economic growth and social impact of faster consolidation. They welcomed, in this context, the authorities’ openness to considering accelerating the pace of fiscal adjustment if upside risks materialized. Directors noted that lowering government spending is essential, especially in areas where expenditure has increased very rapidly over the past several years, notably wages, pensions, and social transfers. They stressed, however, the importance of mitigating the impact of the fiscal rebalancing on the most vulnerable segments of the population.

Directors also encouraged the authorities to continue strengthening the institutional framework for fiscal policy, and welcomed the recent agreement between federal and provincial governments, which should encourage fiscal discipline. They recommended considering the adoption of a medium‑term fiscal anchor and a stronger enforcement mechanism.

Directors welcomed the proposed tax reform, which is a good step forward to overhaul the inefficient tax system. The proposal supports investment, increases the progressivity of the system, and reduces the disincentive to formal employment. Directors noted that more could be done to eliminate distortionary taxes, and cautioned against relying on uncertain growth effects to offset revenue losses from the tax reform.

Directors welcomed the authorities’ commitment to maintaining a tight monetary policy stance in order to achieve their inflation targets. They stressed that reducing monetary financing of the deficit would help strengthen central bank independence and enhance the credibility of the inflation‑targeting regime.

Directors emphasized the need for an ambitious supply‑side reform agenda. They commended the authorities for removing foreign exchange controls and trade restrictions, and for recent initiatives to reduce red tape. They noted that boosting productivity and long‑term growth would require a more accelerated reduction in import tariffs, elimination of most import licenses, removal of barriers to investment and firm entry, and measures to boost domestic competition. Maintaining efforts to fight corruption will also be critical. Directors emphasized the need to continue to develop the financial system and increase financial inclusion, while strengthening oversight and protecting financial stability.

Directors called for measures to reduce informality, address gender discrimination, and ensure that the benefits from higher growth are shared more equally. The proposed tax reform should increase opportunities for formal employment for the less‑educated and young people.

It is expected that the next Article IV consultation with Argentina will be held on the standard 12‑month cycle.

Source: International Monetary Fund

- 329 reads

Human Rights

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

The Peace Bell Resonates at the 27th Eurasian Economic Summit

Declaration of World Day of the Power of Hope Endorsed by People in 158 Nations

Puppet Show I International Friendship Day 2020