IMF Executive Board Concludes Fifth Post-Program Monitoring with Portugal

On February 17, 2017, the Executive Board of the International Monetary Fund (IMF) concluded the Fifth Post-Program Monitoring with Portugal.

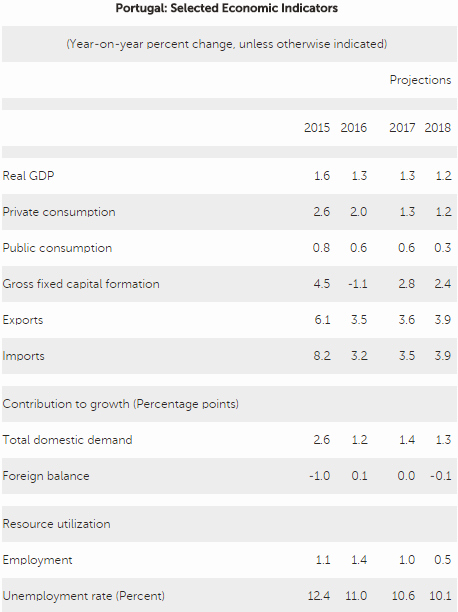

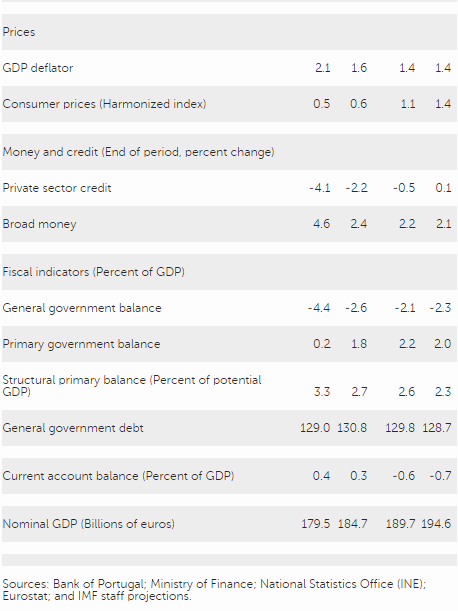

After a sluggish first half, the economy experienced a welcome upturn in growth in the second half of 2016, boosted by stronger exports and a further decline in unemployment to pre-crisis levels. These developments point to an improved near-term outlook, but medium-term growth could be put on a more sustainable footing by reducing structural bottlenecks and high levels of corporate debt. The revised 2016 fiscal target appears likely to have been met, but prospective public outlays for banking sector recapitalization continue to weigh on public debt trends.

Executive Board Assessment

Executive Directors agreed with the thrust of the staff appraisal. They welcomed Portugal’s improved macroeconomic performance in the second half of 2016, marked by a pick‑up in growth, a decline in unemployment, and a fiscal outturn in line with the target. In addition, Portugal has continued to successfully access bond markets and its capacity to repay the Fund is expected to be adequate. Nonetheless, Directors noted that the public debt remains high, and the large annual financing needs, combined with banking system challenges, leave Portugal vulnerable to a range of shocks and a tightening of financing conditions. Directors, therefore, emphasized the need for a stronger momentum to improve financial sector resilience, ensure durable fiscal consolidation, and raise potential growth.

Directors welcomed the recognition by the authorities that continued efforts to improve banking sector soundness are warranted. They stressed that a comprehensive clean‑up of bank balance sheets is essential to break the vicious circle between weak banks, high non‑performing loans (NPLs), and low growth. This should include a predictable, time‑bound, and credible plan for banks to write‑off or restructure non‑performing legacy assets, strengthen internal governance, and improve bank profitability, including by further cutting costs. This would help attract new private capital to support the clean‑up of bank balance sheets. In this context, Directors were encouraged by the authorities’ proposals to address NPLs, including supervisory, legal, and judicial measures to incentivize banks to dispose of non‑performing loans and reduce corporate debt.

Directors welcomed the authorities’ commitment to continued fiscal consolidation and noted their five‑pillar strategy. They underscored the importance of a well‑specified medium‑term fiscal adjustment path that balances the need to put debt on a firmly downward trajectory while supporting growth. They stressed that a fiscal consolidation path that relies more on durable expenditure reform and greater spending efficiency, and less on one‑off measures and capital expenditure compression, would be more sustainable and supportive of growth. They also noted the importance of strengthening the budget process.

Directors underscored that reinvigorating macro‑critical structural reforms remains essential to boost the economy’s competitiveness, growth potential, and resilience to shocks. They encouraged the authorities to proceed with reforms in labor and product markets, with a particular focus on tackling labor market segmentation, improving education and skills, and enhancing public sector efficiency. They noted that it would be important to ensure that increases in the minimum wage do not impair labor competitiveness and undermine prospects for new entrants to the labor force. Removing regulatory barriers, strengthening institutional capacity, and addressing other supply bottlenecks are also considered critical reforms.

Source: International Monetary Fund

- 382 reads

Human Rights

Fostering a More Humane World: The 28th Eurasian Economic Summi

Conscience, Hope, and Action: Keys to Global Peace and Sustainability

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

Puppet Show I International Friendship Day 2020