Design of funded private pensions needs to be improved

Pension systems are changing in response to the challenges they face. Funded Pension arrangements, in particular defined contribution ones, are playing a growing role in complementing retirement income from public sources in OECD countries and worldwide. However, their design needs to be improved, according to a new OECD report.

The 2016 OECD Pensions Outlook analyses how the pensions landscape is changing in the face of challenges that include ageing populations, the fallout from the financial and economic crisis, and the current environment of low economic growth and low returns.

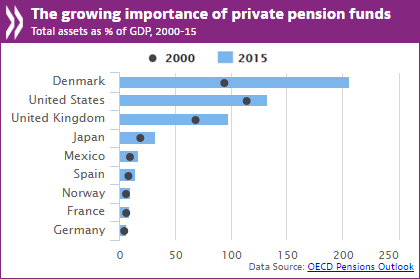

The report shows that there were 13 OECD countries in which assets in funded pensions represented more than 50% of GDP in 2015, up from 10 in the early 2000s. Over the same period, the number of OECD countries where assets in funded private pension arrangements represent more than 100% of GDP increased from 4 to 7 countries.

The increased role of funded pension arrangements mostly comes from defined contributions (DC), pension arrangements in which there is a direct link between contributions, assets accumulated and pension benefits. However, the OECD warns that, although these arrangements have important advantages, they put more of the risks of saving for retirement (e.g. investment and longevity risk) and decision making in the hands of individuals.

”Defined contribution pensions offer some advantages in the current environment of ageing populations, low growth and low interest rates but, as individuals bear more risk and responsibility for managing their retirement finances, we certainly need to focus on improving their design,” said OECD Secretary-General Angel Gurría, launching the report in Paris.

Main policy messages from the Outlook:

● In most OECD countries, the tax treatment of retirement savings provides an overall tax advantage for individuals over their life cycle, but the size of the advantage varies. In at least 20 OECD countries, tax benefits for retirement savings (in relative terms) increase with income. Using flat-rate subsidies and matching contributions can help target assistance towards lower-income individuals and prevent a further widening of inequalities upon retirement.

● A coherent framework for retirement is needed to accommodate and encourage the use of annuity products as they can play an important role in helping individuals mitigate investment and longevity risks. However, increased product complexity heightens the need for appropriate financial advice and comprehensible product disclosures to ensure that consumers purchase products suitable for their needs. It also underlines the need for the regulatory framework to adapt to innovations in product design and encourage appropriate risk management for annuity products.

● Policy makers need to ensure that consumers receive appropriate financial advice for retirement. Measures need to be put in place to ensure that the conflicts of interest that advisors face are mitigated and that advisors are adequately qualified. However, attention also needs to be paid to ensure the continued accessibility and affordability of advice, an area in which technology-based advice can potentially play a role.

● Low financial literacy poses serious challenges, as individuals are increasingly responsible for managing their own retirement wealth. Financial education for retirement planning should be implemented, whilst information about pensions should be available, clear and not overwhelming for individuals; where possible it should be standardised (e.g. costs, fund performance). All information for individuals’ pension plans should be combined and available to use with calculators/simulators in order to provide greater insight.

● In the four OECD countries with separate civil service pension schemes, civil servants’ future pension promises measured in terms of replacement rates are 20 percentage points higher for a full career than those of the private sector. The OECD recommends a pension framework that applies the same rules to the public and private sectors; this should facilitate labour mobility and increase efficiency.

Source: Organization for Economic Co-operation and Development

- 268 reads

Human Rights

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

The Peace Bell Resonates at the 27th Eurasian Economic Summit

Declaration of World Day of the Power of Hope Endorsed by People in 158 Nations

Puppet Show I International Friendship Day 2020