IMF Executive Board Concludes 2016 Article IV Consultation with Portugal

On September 16, 2016, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV Consultation and Fourth Post-Program Monitoring with Portugal.

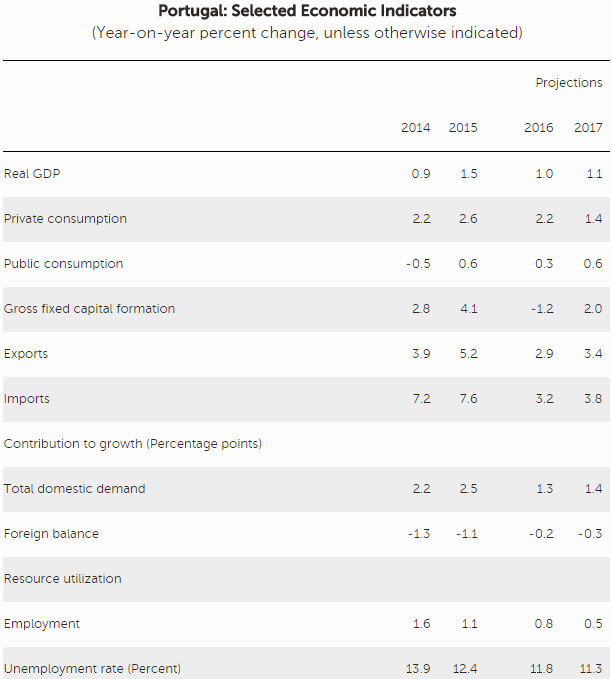

The economic recovery in Portugal is losing momentum. The slowdown in economic activity that began in the second half of 2015 has persisted, despite still-favorable cyclical tailwinds and supportive macroeconomic policy settings. The fiscal loosening in place since last year and the ECB’s appropriately supportive monetary policy stance have translated into robust consumption growth. However, overall GDP growth is being held back by weaker export growth and sluggish investment, with the latter being weighed down by uncertainty, high levels of corporate debt, and still-pronounced structural bottlenecks. Accordingly, output is expected to increase by only 1.0 percent in 2016.

Executive Board Assessment

The Executive Directors welcomed that Portugal has achieved a major economic turnaround since the onset of the sovereign debt crisis, as market access has been restored, fiscal and current account balances have improved, and unemployment, though still high, has fallen substantially. Directors noted, however, that notwithstanding the progress, the recovery is moderating and risks are tilted to the downside. The slowdown in economic activity, together with banking sector vulnerabilities and high public debt, poses challenges. Directors welcomed the authorities’ commitment to address these weaknesses and emphasized that a concerted policy effort, including decisive fiscal adjustment, improvement in banks’ governance, and implementation of key structural reforms, will be critical to strengthening Portugal’s macroeconomic position.

While noting that sovereign financing conditions are subject to global developments, Directors welcomed the staff’s assessment that risks to Portugal’s capacity to repay the Fund remain manageable. In view of the authorities’ intention to repay the Fund early, they underscored the importance of maintaining adequate cash buffers.

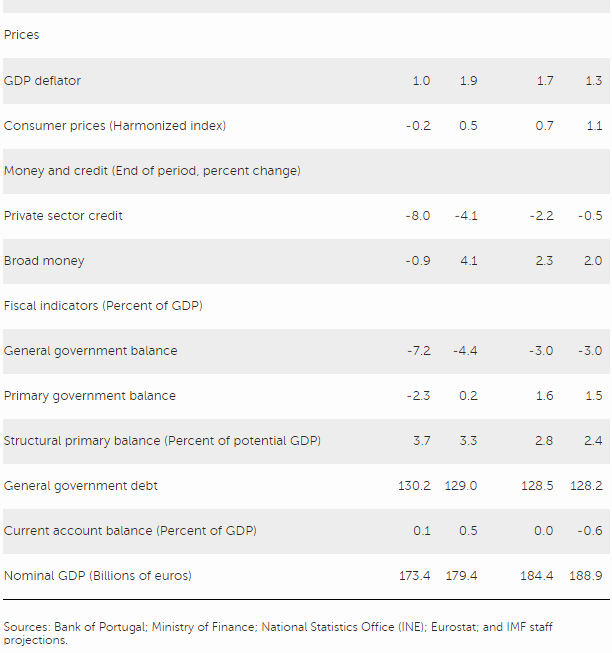

Directors considered the 2016 budget deficit target, 2.2 percent of GDP, to be appropriately ambitious, yet noted the difficulties in achieving this target given declining GDP growth and emerging expenditure pressures. They encouraged the authorities to pursue a well‑specified adjustment path, focused largely on expenditure, that balances the need to put debt on a firmly downward trajectory while supporting growth. Directors called for a comprehensive spending review, aiming particularly at better means‑testing of social benefits and controlling pensions and public sector wages. They also highlighted that tax policy should be more stable and predictable and designed to boost competitiveness and growth.

Directors emphasized that addressing banking sector vulnerabilities should be a top priority. They agreed that to return to profitability and successfully finance economic growth, banks should clean up their balance sheets, including through the tackling of nonperforming loans, supported by an increase in capital and provisions. Directors noted that banks should also reduce operating costs and improve their internal governance to let lending decisions be guided solely by commercial criteria. They also saw merit in finding national‑level solutions to the challenges facing Portuguese banks, using the existing regulatory toolkit.

Directors emphasized that pushing ahead with structural reforms remains critical to enhancing competitiveness and promoting growth. They encouraged the authorities to fully implement the already‑enacted reforms in labor and product markets, with a particular focus on streamlining the functioning of the public sector and limiting energy costs. To support implementation of these reforms, Directors encouraged the authorities to engage all stakeholders by means of an inclusive social dialogue.

Directors welcomed the ex post evaluation of exceptional access under the 2011–14 Extended Fund Facility. The program was a qualified success, given that it helped stabilize the Portuguese economy, but concerns about debt levels remain. Directors generally agreed that the pace of fiscal adjustment had been appropriate; that treating banks as going concerns had been justified in the absence of a banking crisis; and that sovereign debt restructuring had not been a realistic option during the program. Directors pointed to the need for realistic projections and targets, noting in this respect the limits to protecting growth in the face of necessary adjustment. Looking forward, Directors emphasized in particular: the need to develop program modalities and a toolkit for effective adjustment through internal devaluation; the importance of strong forward‑looking banking supervision and a proactive approach to private sector deleveraging; the need to handle effectively legal constraints in program design; and the key role of country ownership in all branches of government to enable and sustain reforms.

Directors recognized the determinative role of EU support in Portugal’s recovery and current stability. For the effective design of future Fund programs with members of currency unions, most Directors considered that high priority should be put on clarifying options for union‑level conditionality, and for instruments to ensure that member countries’ program goals can be met in the face of asymmetric shocks not easily resolved by union‑wide monetary policy.

Source: International Monetary Fund

- 297 reads

Human Rights

Fostering a More Humane World: The 28th Eurasian Economic Summi

Conscience, Hope, and Action: Keys to Global Peace and Sustainability

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

Puppet Show I International Friendship Day 2020