IMF Executive Board Concludes 2016 Article IV Consultation with Peru

On June 20, 2016, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Peru, and considered and endorsed the staff appraisal without a meeting.

As a result of prudent macroeconomic management, Peru has successfully navigated the commodity cycle and the 2008–09 global financial crisis, and still leads growth among large Latin American economies. Thus, the new government, which takes office on July 28, 2016, will inherit an economy with a solid foundation, good institutional frameworks in place, and structural reforms in train.

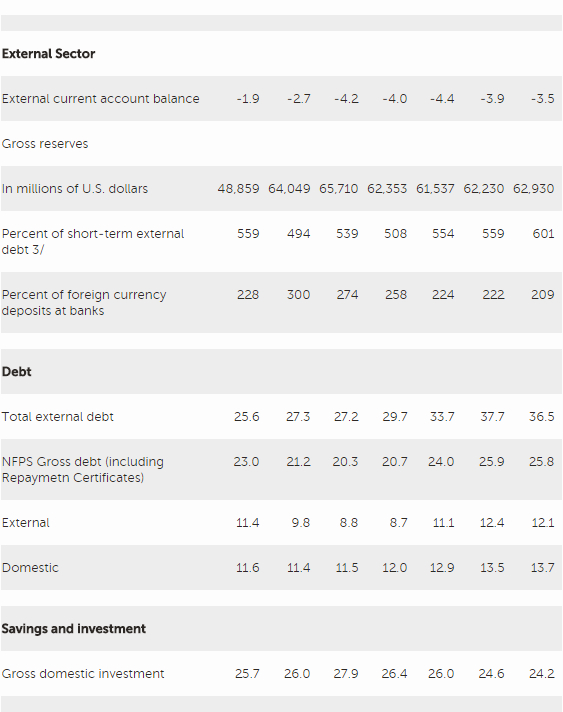

However, important challenges now loom, as metal prices have entered into a slump since their 2011 peak, hurting exports, investment, and fiscal revenues. Following a sharp and unexpected drop in 2014, growth picked up in 2015, reaching 3.3 percent largely owing to higher metals production and fishing, and a partial recovery in services and commerce. Despite a widening negative output gap, inflation increased by more than 1 percentage point to 4.4 percent, y-o-y, in December 2015, reflecting food supply shocks, regulatory adjustments to energy prices, and a pass-through from currency depreciation. The external current account reached a deficit of 4.4 percent in 2015 despite the sol depreciation.

Monetary and exchange rate policies remained attentive to rapidly changing conditions. The central bank has raised the policy rate since September 2015 by a full percentage point to 4.25 percent aiming at re-anchoring inflation expectations, which has added to tighter external financial conditions. The sol was allowed to depreciate 14 percent with respect to the U.S. dollar, while volatility was contained. The authorities have eased the adjustment to commodity price shocks through an expansionary fiscal policy in 2015, but with mixed results, as capital spending continues to suffer delays.

Peru is positioned to grow faster in the next two years, as mining production reaches full capacity and large infrastructure projects advance. Inflation is expected to decline. Risks to the outlook are balanced, and downside risks are mostly on the external side. Upside risks on the domestic front are a pick-up in sub-national investment and possible larger-than-projected increases in confidence and investment after the presidential election.

Executive Board Assessment

After decelerating sharply in 2014, economic activity recovered last year despite a volatile external environment. The recovery largely reflected additional mining production capacity coming on stream, although non-mining activity has also accelerated modestly more recently. An expected increase in mining exports, together with some rebound in public investment, will impart a strong positive impetus on growth going forward, which should spillover to non-commodity sectors. Thus, despite sluggish external conditions, activity is expected to accelerate further in 2016 and 2017, while inflation continues to decline.

Risks to the outlook are balanced. External pressures have carried over from last year and comprise possibly weaker-than-projected growth in China (and, hence, softer metal prices), possible adverse spillovers from other countries in the region (though these should be relatively small), sharp asset price adjustments in advanced and emerging economies, and an even stronger dollar. The response to shocks should be through further exchange rate flexibility and easing liquidity conditions to support credit activity. Upside domestic risks include stronger-than-expected improvements in business confidence (especially if the incoming government announces decisive productivity-enhancing reforms) and a more effective execution of the existing pipeline of infrastructure projects, which could lift growth further in 2016–17 and beyond.

Monetary and exchange rate policies should remain attentive to rapidly changing conditions. Following monetary tightening, the BCRP should now maintain a wait-and-see stance—given declining inflation and medium-term inflation expectations, the fact that it is too soon to evaluate the effect of past monetary tightening on economic activity and inflation, and the usual uncertainties surrounding the exact cyclical position of an economy. This said, a possibly steeper interest rate path in the United States than currently priced by the financial market could trigger the need for further monetary tightening in Peru. Greater exchange rate flexibility in 2015 was a welcome development with no noticeable impact on firms’ and banks’ balance sheets; the latter remain healthy and profitable. Further decline in credit de-dollarization has been achieved not least due to the measures introduced by the BCRP. Further exchange rate flexibility would support the development of hedging instruments to reduce currency risk and help accelerate the de-dollarization process. Recent measures to deepen Peru’s equity market are also welcome.

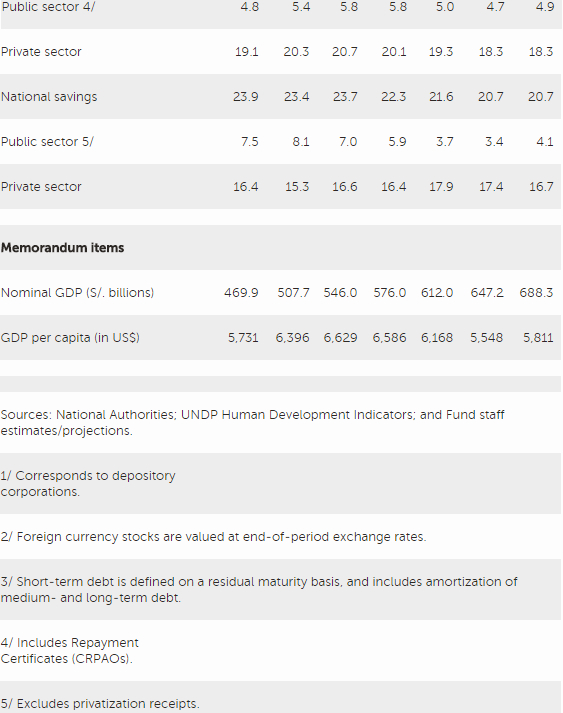

A gradual fiscal consolidation in the next few years is advisable to maintain healthy debt dynamics and to protect fiscal buffers. With the output gap closing around end 2017, there is no case for loosening fiscal policy. A gradual fiscal consolidation would be important for ensuring the sustainability of pensions, and defending against natural disasters and realization of contingent liabilities. To accommodate higher-than-projected public capital spending, it will be critical to create adequate fiscal space through containing current spending that is not complementary to capital expansion and structural reforms (including in health and education), and raising the low revenue collection through streamlining administration, reducing informality and exemptions, and protecting Peru’s tax base from possible international profit shifting by multinational corporations. Reducing bottlenecks to public investment and improving management would go a long way toward enabling full execution of budgeted spending and would support private investment.

With the end of commodity-driven growth, the agenda for growth-spurring structural reforms has become a higher priority, including for further poverty reduction. Investments in capital and labor will be needed to boost potential growth, which is otherwise estimated to be 3.5 percent in the absence of continued reforms. Long-standing challenges include reducing informality, which should be in part addressed through labor market reforms aiming at lowering the costs of hiring and firing workers, and spurring investment in non-extractive industries, including through improving competitiveness and infrastructure. Peru’s current decentralization framework should be improved, as it constrains full execution of planned capital expansion and better allocation of resources. While Peru has achieved one of the highest rates of education coverage in Latin America, the low quality of education remains a crucial challenge, and the ongoing reforms will need to continue. Efforts to raise financial inclusion are commendable, especially through the launch of the broad-based National Financial Inclusion Strategy and the private sector-led e-money platform. Free trade agreements also provide an opportunity for boosting and diversifying long-term growth.

Source: International Monetary Fund

- 321 reads

Human Rights

Fostering a More Humane World: The 28th Eurasian Economic Summi

Conscience, Hope, and Action: Keys to Global Peace and Sustainability

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

Puppet Show I International Friendship Day 2020