IMF Executive Board Concludes 2014 Article IV Consultation with the Democratic Republic of the Congo

On June 9, 2014, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with the Democratic Republic of the Congo.

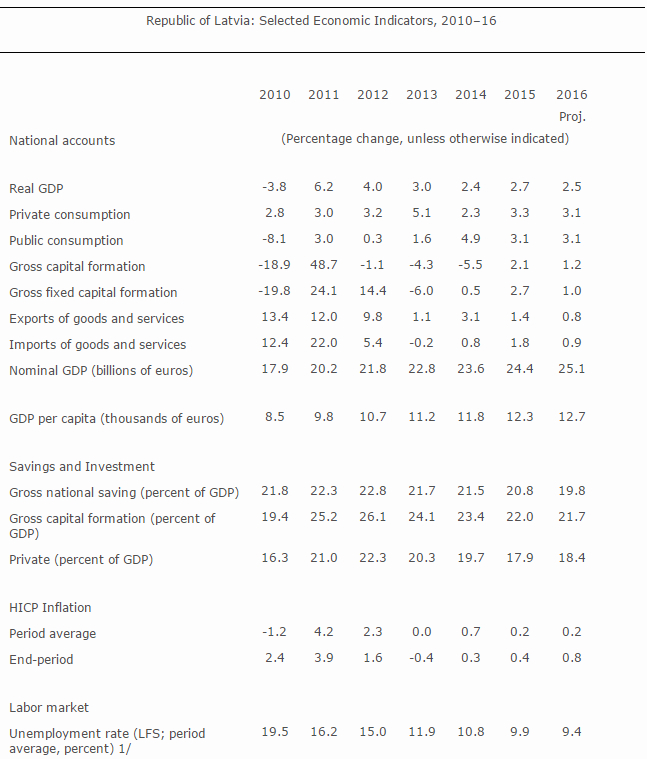

The Democratic Republic of Congo (DRC) has continued to post strong economic growth in the recent years (7 percent on average for 2010–12) despite the difficult domestic security situation. Mineral production and related investments have become the main drivers of the robust growth, although economic activity is strengthening in other areas such as the agricultural sector resulting into a real gross domestic product (GDP) growth rate of 8.5 percent in 2013. Fiscal restraint and the absence of major external price shocks helped to further reduce inflation to a record low of 1 percent at end-2013. Higher mining exports and sustained inward foreign investment contributed to an overall balance of payments surplus. However, gross international reserves increase in 2013 was only sufficient to keep the reserve coverage at 7.7 weeks of non aid related imports of goods and services, which remains low although the exchange rate remained remarkably stable since 2010.

Notwithstanding the strong economic growth, poverty remains pervasive and the economy vulnerable. Limited fiscal space and shocks to revenues often offset by expenditure adjustments have not supported pro-poor and critical investment spending necessary for inclusive growth, giving rise to mounting social demands to share in the benefits of the accelerating growth.

Progress in structural reforms was mixed. The government implemented important reforms aimed at de-dollarizing the economy, deepening financial markets and improving public finance management (PFM). The Central Bank of Congo (BCC) successfully initiated the introduction of new denominations of the Congolese Franc and the government expanded public salary payments through banks for most civil servants. Reforms in PFM also progressed with improvements in the expenditure chain and a reduction of the expenditure float. In contrast, structural reforms to further the independence of the BCC, including through its recapitalization, and to improve transparency and governance of state-owned enterprises (SOEs) in the mining sector largely stalled.

Medium-term economic growth prospects remain favorable. The economy is projected to grow at 8.7 percent in 2014 and on average 7.5 percent during 2015–18. The mining sector is expected to remain the main driver of growth, including with the investment phase of the Sino-Congolese joint venture (Sicomines) accelerating. Inflation is projected at 4 percent in 2014, which appears achievable in light of current low inflation, the BCC sterilizing any excessive liquidity and in the absence of foreign price shocks. A drop in the international prices of the DRC’s main mineral exports export represent the main risk to the DRC’s economic outlook.

Directors commended the authorities for maintaining macroeconomic stability in the face of a challenging external and domestic environment, but noted that notwithstanding the recent strong economic growth, poverty remains widespread and the attainment of the Millennium Development Goals (MDGs) is at risk. Directors welcomed the recent positive developments on the security front and encouraged the authorities to use this window of opportunity to consolidate recent macroeconomic gains and step up the pace of structural reforms needed to promote diversified, sustainable and more inclusive growth.

Directors emphasized the importance of creating fiscal space to increase priority social spending and support public investments for meeting the MDGs, through improvements in public financial management, better alignment of the budget with the Poverty Reduction Strategy Paper, and strengthened domestic—including non-resource—revenue mobilization. In this regard, they called for improved tax administration, including by addressing known VAT shortcomings, tighter control of the tax base, and greater efforts to raise the contribution of the mining sector to the budget.

Against this backdrop, Directors called for improved governance and transparency and strengthened oversight of state-owned enterprises (SOEs) in the mining sector. Corrective actions in this area could help pave the way for discussion of a possible successor arrangement. Directors underscored the need to accelerate reforms, including the adoption of a mining code and petroleum law aligned with international best practices, and encouraged full compliance with the Extractive Industry Transparency Initiative (EITI) and the adoption of an improved anti-money laundering framework. In this regard, they recommended more effective management of tax mining assets to avoid SOE revenue losses in the natural resource sector.

Directors called for critical reforms at the Banque Centrale du Congo (BCC) to bolster its operational independence and accountability, strengthen its capacity to conduct monetary policy, sustain price and financial sector stability, and instill market confidence. In this context, they welcomed the authorities’ adoption of a three-year action plan incorporating the Financial Sector Assessment Program (FSAP) recommendations. They advised swift implementation of key policy measures—including, recapitalizing the BCC, adoption of the draft law of the statutes of the BCC and the Banking Law, and divestment of noncore activities. The analytical, regulatory and supervisory capacity of the BCC should also be strengthened.

Directors called for enhanced exchange rate flexibility in order to set the stage for a more ambitious accumulation of international reserves, designed to help enhance the economy’s resilience to exogenous shocks and further strengthen market confidence, especially given the authorities’de-dollarization strategy.

1. Starting in 2012 CPI numbers is calculated by INS using a revised methodology. The CPI for 2012 according to the previous methodolgy amounted to 5.7 percent (eop) and 9.3 (average).

2. The projections for 2011 and beyond account for mining companies profit outflows.

3. Projections are based on calculations under the 2010 HIPC Debt Sustainability Analysis (EBS/10/121, 06/16/2010). Includes assistance beyond the terms of the enhanced HIPC Initiative granted by some Paris Club creditors. Exports are a trailing three-year moving average.

Source: International Monetary Fund

- 332 reads

Human Rights

Ringing FOWPAL’s Peace Bell for the World:Nobel Peace Prize Laureates’ Visions and Actions

Protecting the World’s Cultural Diversity for a Sustainable Future

The Peace Bell Resonates at the 27th Eurasian Economic Summit

Declaration of World Day of the Power of Hope Endorsed by People in 158 Nations

Puppet Show I International Friendship Day 2020